04/02/2017

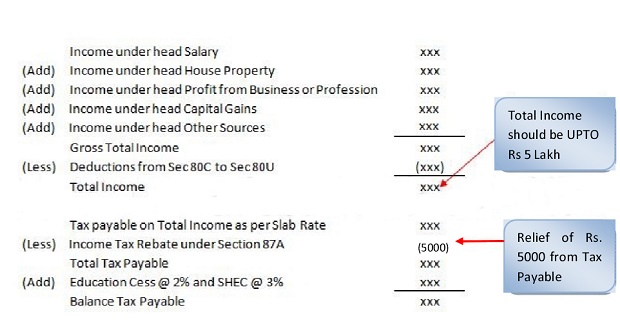

Rebate of up to Rs. 5,000 for resident individuals having total income of up to Rs. 5,00,000 as per Sec-87A of Income Tax Act, 1961 for A.Y. 2017-18 i.e. F.Y. 2016-17.

The rebate shall be equal to the amount of income tax payable on the total income for assessment year 2017-18 or an amount of Rs. 5,000, whichever is less.

Key Point :-

- Individual resident of India,

- Whose Total Income is up to Rs. 5,00,000,

- Shall be allowed a rebate, From Income Tax,

- 100% of Income Tax or Rs.5,000, Whichever is Less.

The above points have been represented below showing the manner of Computation:-

Example 1

Compute the tax liability of X Ltd., a domestic company, assuming that the total income of X Ltd. Is Rs. 2,80,000.

Answer

| Particulars | Rs. |

| Tax on total income@30% of Rs.2,80,000 | 84,000 |

| Less: Rebate under section 87A* | ( – ) |

| 84,000 |

| Add: Education cess@2% | 1,640 |

| Secondary and higher education cess@1% | 840 |

| Total tax liability | 86,480 |

*As per section 87A the rebate of Rs. 5,000 is allowed to residential individual.

Example 2

Compute the tax liability of Mr. X, a salaried employee (age: 45 years), assuming that the total income of Rs. 4,80,000. During the previous year ending on March 31, 2017.

Answer

| Particulars | Rs. |

| Tax on total income@10% of Rs.2,30,000

(Rs.4,80,000-2,50,000) | 23,000 |

| Less: Rebate under section 87A | (5,000) |

| 18,000 |

| Add: Education cess@2% | 360 |

| Secondary and higher education cess@1% | 180 |

| Total tax liability | 18,540 |

*As per section 87A the rebate shall be equal to the amount of income tax payable or an amount of Rs. 5,000, whichever is less.

Example 3

Compute the tax liability of Mr. X, a salaried employee (age: 45 years), assuming that the total income of Rs. 2,60,000. During the previous year ending on March 31, 2017.

Answer

| Particulars | Rs. |

| Tax on total income@10% of Rs.10,000 | 1,000 |

| Less: Rebate under section 87A | (1,000) |

| Add: Education cess@2% | Nil |

| Secondary and higher education cess@1% | Nil |

| Total tax liability | Nil |

*As per section 87A the rebate shall be equal to the amount of income tax payable or an amount of Rs. 5,000, whichever is less.

- 10000*10% = 1000

- 5000

Rebate allowed of Rs.1000.

Example 4

Compute the tax liability of Mr. X (age: 45 years), assuming that the total income of Rs. 5,40,000. During the previous year ending on March 31, 2017.

Answer

| Particulars | Rs. |

| Tax on total income@10% of Rs.2,90,000 | 29,000 |

| Less: Rebate under section 87A | (- ) |

| 29,000 |

| Add: Education cess@2% | 580 |

| Secondary and higher education cess@1% | 290 |

| Total tax liability | 29,870 |

No Rebate U/s. 87A is allowed as Total Income Exceeds Rs. 5,00,000/-

*As per section 87A the rebate shall be equal to the amount of income tax payable or an amount of Rs. 5,000, whichever is less.

Example 5

Compute the tax liability of Mr. X, a salaried employee (age: 45 years), assuming that his casual income of Rs. 4,80,000. During the previous year ending on March 31, 2017.

Answer

| Particulars | Rs. |

| Tax on total income@30% of Rs.4,80,000 | 1,44,000 |

| Less: Rebate under section 87A | (5,000) |

| 1,39,000 |

| Add: Education cess@2% | 2,780 |

| Secondary and higher education cess@1% | 1,390 |

| Total tax liability | 1,43,170 |

*As per section 87A the rebate shall be equal to the amount of income tax payable or an amount of Rs. 5,000, whichever is less.

|

About the author

vijay rai

ACCOUNTS AND TAX CONSULTANTS

|

Print